![<?echo $_SERVER['SERVER_NAME'];?>](/template/twentyseventeen/skin/images/header.jpg)

Hot spot funds flow to thousands of stocks to evaluate stocks to diagnose the latest rating simulation transaction

Client

1, cockroaches: internal strong and weak, strong soybeans and weak vegetables

The CBOT soybean market was mixed in October. The market expects that the supply and demand report for October will further increase the possibility of yield and production. Harvest pressure will be reflected. From a time perspective, the US Department of Agriculture reported that before October 12, the market may be weak, and harvesting lows may occur. With the digestibility of production, the late South American sowing weather and the export of US beans will support prices. For the domestic cockroach market, before the beginning of October, due to the long holiday and the 19th National Congress, some oil plants will be shut down, and soybean meal stocks will be reduced. Relatively speaking, since October is the weakest month for the consumption of rapeseed, the pattern of strong soybeans and weak vegetables will be highlighted. Relatively speaking, soybean meal is stronger than the vegetable meal, and the overall protein market is strong and weak; the soybean meal is strong and the vegetable is weak.

2, oil: stock pressure is greater than weak market, palm oil production rhythm changes are worthy of attention

Due to the frequent changes in the relevant policies of biodiesel in the United States, the market is also intensifying the divergence of future consumption expectations of US soybean oil. The Malaysian palm oil supply and demand report released in October became the key. If the Malaysian palm oil production dropped significantly in September, it means that the palm palm oil entered the production cycle ahead of schedule and the supply pressure was released. In contrast, domestic oil market inventory pressure remains evident in October, soy oil stocks may fall, but palm oil and rapeseed oil may increase. However, due to the steady domestic demand for oil in October. The oil and fat market destocking process is slow. Relatively speaking, due to the upside down of palm oil, there is still a gap in supply. Once the purchase is insufficient in the later period, it will boost the oil market.

3, strategy recommendation

Unilateral strategy: As the State Reserve temporarily stopped shooting soybeans, the previous soybean transaction rate was high, indicating that the soybean market price is more recognized, and soybeans will show a strong operation. It is recommended that investors treat the apes market in a range operation and operate in the interval band. Mainly. Grease is running weakly, paying attention to changes in rhythm.

Arbitrage strategy: You can buy bean empty operation; palm oil is stronger than soybean oil, and it is stronger than the future. Soybean oil is the opposite; this can be considered to buy palm oil near the moon and the moon, soy oil to buy near the moon and the moon.

Option strategy: In the medium and long term, we can also consider the strategy of doing more volatility.

Future market concerns: South American planting schedule and weather, North American sales progress, domestic oil plant crushing rhythm, Malay palm oil production inventory.

First, the market review

The weather conditions of US soybean cultivation are good. The market expects the possibility of high yield of Meidou to increase. The increase in yield and the strong influence of exports are superimposed. The long and short factors are intertwined, and the market for apes maintains a wide range of fluctuations. Oil and fat inventories have rebounded, consumer expectations have gradually been digested by the market, and the price support kinetic energy has weakened. Oil prices have entered the downward channel, and the pattern of oil stagnation has changed.

In September, the USDA monthly supply and demand report once again unexpectedly increased the yield, and the US soybean new crop production was again raised to 4.431 billion pu, which was higher than market expectations and formed a certain suppression on CBOT soybeans and domestic scorpion prices. The latest quarterly grain inventory report showed that US soybean stocks increased year-on-year, but overall the overall results were less than expected. Judging from the current weather conditions of the US soybeans, rainfall in the central and western parts of the United States improves soil moisture, and the possibility of high yields in the US soybeans is higher. If the rains in the Midwest are good in early October, the yield of US beans will increase further. Horse palm oil has recently exported strongly. In September, the export volume was 1,384,665 tons, an increase of 10% from the previous month. With the support of weaker RM, the performance of palm oil was stronger than that of soybean oil and vegetable oil. Later, it is recommended to pay attention to the USDA October supply and demand report, US soybean export data, South American soybean planting, MPOB Malay palm oil production and inventory.

Table 1: Monitoring Table for Important Indicators of Grease and Oil Main Contracts (Monthly Data)

Source: Great Futures Institute, Wind

1CBOT soybean closing price unit is cents / pu

Second, the basic analysis of oil supply and demand

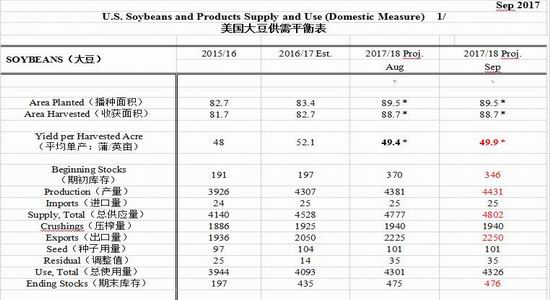

1. USDA September monthly supply and demand report: affecting the short-selling

After the US Department of Agriculture reported an increase in yields in August, it unexpectedly increased its yield to 49.9 bushels per acre in the September report. The US soybean new crop production was again raised to 4.431 billion pu, higher than market expectations and a record high. The price of CBOT soybeans and domestic soybean meal fell. According to the statistics of the mainstream analysis institutions in the past five years, whether it is Informa or FCSTone, its US soybean yield estimates for August-September are lower than the final yield of US beans. This year's US soybean crop yields continue to rise unexpectedly, indicating that the dry weather in July-August has relatively limited impact on the growth of US soybeans. At the same time, with the improvement of the biotechnology of the US soybean varieties, the yield level of soybeans and their ability to resist drought and cold have also improved. If the early frost in the US soybean harvest period is not serious, it is expected that the yield of US soybeans will further increase in the later period.

Table 2: USDA September Monthly Supply and Demand Balance Sheet (US Soybean)

Source: Great Futures Institute, US Department of Agriculture

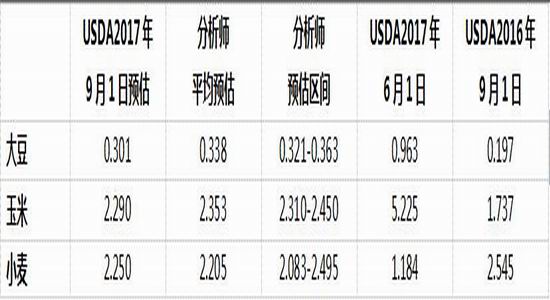

2, quarterly grain inventory report: inventory is less than expected, the impact is more

In the early morning of September 30th, Beijing time, the US Department of Agriculture released a quarterly grain inventory report. As of September 1, US soybean stocks are expected to be 301.3 million bushels, up from 196.7 million bushels in the same period of 2016, but lower than the market consensus. The value is 339 million bushels, and the impact is excessive.

Table 3: USDA Quarter Grain Stock Report (Unit: 1 billion bushels)

Source: Great Futures Institute, US Department of Agriculture

3, the US soybean harvesting weather: pay attention to early frost phenomenon

In previous years, the first frost period in the United States was at the end of September and early October. This year, the mid-western soybean season in the United States suffered from heavy rains, and many major soybean producing states replayed or delayed planting, which delayed the harvest of the US soybeans. This makes the probability of encountering early frost in the harvest of the US beans greatly increased. If the early frost phenomenon occurs, it will cause the crop to stop grouting, and the quality and yield of the US soybean will be greatly affected. The market is more concerned about this. However, as far as the current weather conditions in the United States are concerned, there has not been any substantial early frost effect, and it is expected that the yield of US soybean yields will be limited.

Figure 1: Informa, FCSTone estimates and final crop yields in September 2013-September 2017

Source: Great Futures Research Institute, Huiyi

4, South American soybean supply: Chen Zuo squeezed the US soybean market, the new crop planting weather caused concern

As the US soybeans enter the harvesting period, the new crops will gradually be transformed into effective supply in the market, which will compete with the old crops of South American soybeans. The scale of US soybean export sales will also depend on the US and Brazil's export discounts to China. Competitiveness. Due to the continued strong exchange rate of the previous Real, farmers are reluctant to sell, and South American soybean sales are not smooth. At present, there are still 55 million tons of South American stocks (35 million tons of Argentine beans and 25 million tons of Brazilian beans). The real exchange rate has stabilized in the 3.1-3.2 range recently. The sales income of farmers has increased compared with the previous period. Brazilian soybeans will further squeeze the US soybean export market, but the risk of Brazilian politics is still unstable, and it needs to be paid attention to this.

In November, South American soybeans will enter the early sowing period. Next, the planting weather in South America will gradually attract market attention. Recently, the US Center for Climate Prediction (CPC) released a report saying that the probability of forming a La Niña phenomenon from November 2017 to January 2018 was 62%, higher than the 26% predicted last month. The center subsequently issued an early warning of the La Nina phenomenon. If the trend of Ranina continues, it will lead to drought in parts of Brazil, which will lead to the production of soybeans in South America.

5, US soybean exports: US beans to buy a ship to increase data strong support period price

According to customs data, China imported 8.45 million tons of soybeans in August 2017, although it fell 16.2% from the previous month, but still set a record high in the same month, higher than market expectations.

The increase in China’s purchases has made the US soybean export momentum particularly strong. According to the latest data released by the US Department of Agriculture, as of the week of September 21, the net sales of US soybean exports was 2,982,700 tons, which exceeded market expectations again (previously the market expected value was 1.8-2.2 million tons), which lasted for several weeks. Strong export momentum. This year's US soybean growth period, the overall weather is good, in this case, the support role of US soybean export data on the price has gradually emerged.

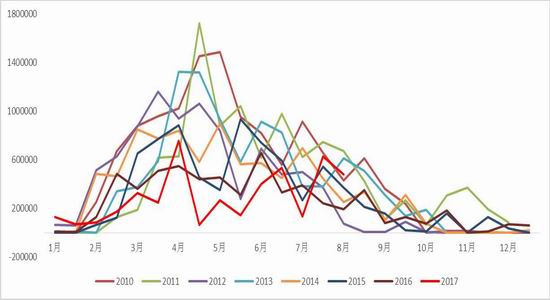

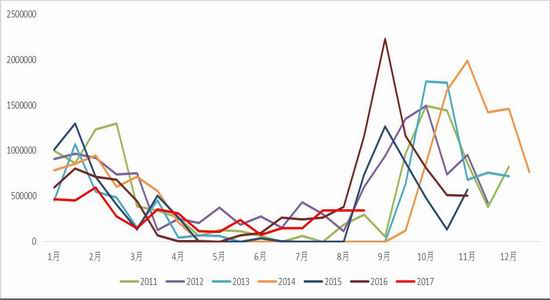

Chart: Brazilian soybean seasonal exports (shipment quantity)

Figure: US soybean seasonal exports (shipment quantity)

Source: Great Futures Institute, Wind

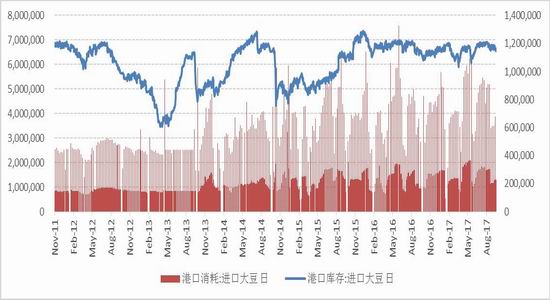

6, domestic soybean crush: soybean pressure to Hong Kong is greater than the demand for continuation

Recently, domestic soybean arrivals and soybean meal inventory pressures continue to decrease. Near the National Day holiday, the department's oil plant shutdown plan was extended in October, and the downstream terminal's stocking schedule was advanced, and the delivery speed was accelerated.

Figure: Number of soybean imports

Chart: Port soybean consumption and stocks

Source: Great Futures Research Institute, General Administration of Customs

Recently, the oil mills continue to recover, and the domestic market is more inclined to trade the soybean meal delivery expectations. Most factories mainly implement contracts. In terms of inventory, as of September 24, the port soybean meal inventory was 711,500 tons, which has fallen to the historical median range.

Figure: Oil mill press operating rate

Figure: Domestic oil mill crush profit

Source: Great Futures Institute, Wind

7, downstream pig breeding: live pigs are still in the low downstream feed demand is difficult to recover in the short term

According to data monitored by the Ministry of Agriculture, the live pig stocks continued to fall in August, and the demand for pigs in the pig industry suffered resistance. According to the latest data released by the Ministry of Agriculture, the live pig stocks continued to decline by 0.5%, down 5.6% year-on-year, and the growth of sows fell by 0.9% from the previous month, down 4.7% year-on-year, and the decline continued to expand.

Third, the analysis of the fundamentals of oil supply and demand

1. The current price of oil and fat is falling back and adjusted

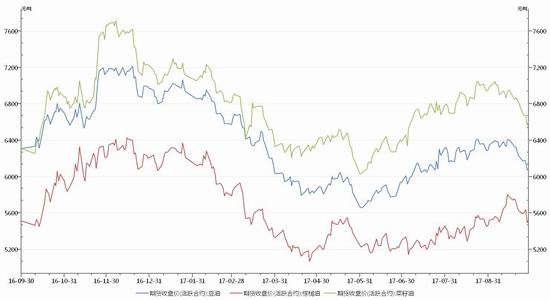

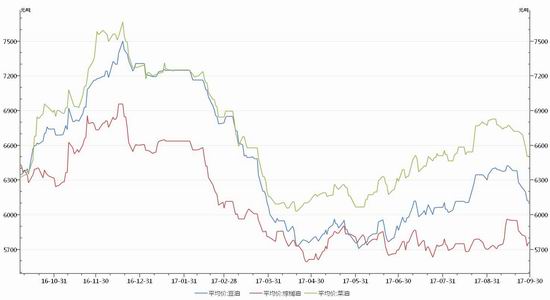

This month, the oil and fat market showed a trend of falling back. The three major oils did not continue to rise on the basis of the increase in August. The spot price of palm oil was firm, followed by vegetable oil and soybean oil. Futures prices lead palm oil, followed by vegetable oil and soybean oil. After the USDA September supply and demand report was released, the trend of the cockroaches was sideways and the oil rushed back. From the current market point of view, the medium-term oil trend showed a downward adjustment pattern, and the expectation of rising in the fourth quarter still exists.

Figure 11: Three major vegetable oil futures price trends

Figure 12: Three major vegetable oil spot price trends

Source: Great Futures Institute, Wind

2, US soybean oil stocks fell, the firewood policy changes around the market

The USDA September report continued to reduce US soybean oil stocks to 830,000 tons in 2016/17, and USDA has lowered US soybean oil stocks for 2016/17 for three consecutive months. As a result, the 2017/18 US soybean oil stocks were also lowered three times in a row, and the September estimate was at 800,000 tons. The main reason for the decline in inventories came from the increase in domestic consumption in the United States, especially in 2017/18, where industrial consumption increased significantly. From the perspective of annual stocks, US soybean oil stocks have fallen. From the monthly inventory, the latest published NOPA report data shows that US soybean oil stocks fell from 820,000 tons in April to 640,000 tons in August. It can be seen that for the United States, its soybean oil presents an obvious destocking situation.

For biodiesel of US soybean oil, it can be said that the policy is changeable and mixed. The US Department of Commerce announced on August 22 that it would impose 50%-64% and 41%-68% of countervailing duties on Argentina and Indonesia biodiesel, respectively, due to subsidies. The market is expected to increase the consumption of US soybean oil in the later period. However, the US Environmental Protection Agency said on September 19 that it is seeking public comment on reducing the use of renewable fuels in 2018 and 2019. If the public agrees to lower the price, then the amount of biodiesel used in the US soybean oil may be variable. Its 2017/18 inventory may pick up, and the US biodiesel policy in October is particularly important.

3, palm oil Malaysia production is less than expected, fear of cutting production ahead of schedule

In August, September and October, the peak period of horse palm oil production is reached. After October, it will enter the production reduction cycle. It will end in October and start to reduce production in November, or slightly ahead of schedule. Judging from the recovery of Malaysian palm oil production in 2017, there is a big difference from market expectations, far below market estimates. According to the August report released by the Malaysian Palm Oil Board, Malaysia's palm oil production in August decreased by 0.9% from July to 1.81 million tons. At the same time, due to strong exports, Malaysian palm oil stocks in August were lower than 2014 and 2015 levels. From this point of view, the increase is limited. For the September report, palm oil production fell 0.8% on September 1-25, according to current production data from the Southern Palm Oil Millers Association. From the rainfall in Malaysia, the low rainfall in Malaysia from June to July will have an impact on palm oil production in two months. From now on, the growth of horse palm oil production in August and September is less than expected, which is related to Insufficient rainfall in the first two months. Due to the decline in production in September, Malaysia is likely to enter the production cycle ahead of schedule. Due to the weakness of the Malaysian currency Ringgit and the strengthening of the previous US soybean oil, the international soybean oil and palm oil price rebounded, which made the horse palm oil export began to pick up. According to the latest ITS report, September 1-25, the horse palm oil exports were exported. The increase was 16.1%. The decline in production and the increase in exports. This has pushed back the increase in seasonal stocks of horse palm oil. If the late MPOB data shows that the output is less than expected, this will boost the horse palm oil. If Malaysia enters the production cut-off cycle ahead of schedule in October, the market supply pressure will weaken in the later period, which will also boost palm oil prices.

4. Domestic soybean oil stocks remain high

At present, domestic oil and fat inventories are still at an absolute high level, and the supply pattern has not changed much from last month. As of September 26, domestic soybean oil stocks were about 1,432,200 tons, slightly higher than the previous month's 1.41 million tons, an increase of 10% from 1.88 million tons in the same period of last year, and an increase of 12% from the same period of the same period of 1.16 million tons. The national port palm oil inventory was around 322,000 tons, down 3.6% from 334,000 tons in the same period last month, 5.6% from the 337,500 tons in the same period last year, and 56.7% from the 700,000 tons in the past three years. Since June, domestic palm oil stocks have continued to decline, and the number of imports has continued to decline due to the obvious import inversion. The inventory of domestic vegetable oil and oil plants was 199,000 tons, slightly lower than the 219,000 tons last month, a significant increase of 30% from the 153,000 tons in the same period of last year. It was still affected by the preliminary auction of vegetable oil. The current domestic vegetable oil stocks are still in the history. On a high level. With the depletion of the vegetable oil, the main supply of the domestic vegetable oil market will be concentrated on the pressing of imported rapeseed. The purchase price of domestically produced rapeseed continues to rise this year. The cost of domestic rapeseed pressed vegetable oil is over 10,000 yuan, which greatly exceeds the cost of imported rapeseed pressed vegetable oil. The market expects that the supply of rapeseed will be reduced in the later period, which will boost the price of vegetable oil. From the inventory point of view, due to the increase in the operating rate of soybean oil, the inventory increased significantly. The vegetable oil in the early stage of the vegetable oil is still in the digestive period. Due to the current decline in the operating rate of rapeseed, the stock of vegetable oil may slowly fall back. As a result of the sharp decline in imports of palm oil, stocks have steadily declined. At present, the pressure of oil supply is from soybean oil, vegetable oil and palm oil. The order of strong and weak relationship is palm oil, vegetable oil and soybean oil.

5. The overall loss of domestic oil import prices

In August, the import of oils and fats reduced the overall premium of domestic prices, and the import losses gradually eased, which led to the gradual preparation of the corresponding varieties of oil imports. Compared with the end of last month, the loss of imported soybean oil has been reduced, but the discount is still deeper; the import of palm oil and vegetable oil has risen and fallen, and the profit of palm oil has increased significantly from the end of last month. The main reason is that the import price has dropped by a large margin; The profit of vegetable oil is the increase in import costs and the decline in import profits. At present, domestic palm oil imports are limited, but once imports are profitable, the total import volume will increase rapidly. At present, the domestic inventory of palm oil will gradually be rebuilt.

Table 4: Three major oil import profit tables

Source: Great Futures Research Institute, Huiyi

Table 5: Three major oil import income statement

Source: Great Futures Institute, Wind

6, beans, brown, vegetable oil price fluctuations change temporarily brown oil is stronger than beans, vegetable oil

From the fundamental factors, the difference between the three major oils of beans, palms and vegetables is mainly caused by the fluctuation of palm oil and beans and vegetable oil. The first half of the month is mainly diffuse, and the middle and late September converge. Palm oil stocks fell slowly compared to the same period last year. Soybean stocks will run at high levels, but stocks will increase slowly. In addition, the market's impact on the market after the release of the national reserve vegetable oil is expected to be reduced, provided that the national reserve vegetable oil auction will not be restarted immediately.

Chart: Soybean oil and palm oil price trend

Source: Great Futures Institute, Wind

Therefore, for October, the price difference between bean and brown will still be dominated by shock convergence. Seasonal regression can be involved in short-term intervention, rapid changes in spreads, and attention to the rhythm of price changes. In terms of bean and vegetable, the price of vegetable oil was once strong, and it was arranged in the middle among the three varieties of oil. However, due to the excessive increase in prices last month, the trend of the beans was still slightly reduced. The price difference of brown vegetables is still dominated by shock convergence. The change in price difference is mainly based on the price change between oils and fats. Mastering the short-term rhythm is the key point.

The oil and fat market is still affected by the weather of the US soybeans. At present, the weather is partially improving and the market is under pressure. In view of the function of oil rotation, the oil may be supported by the staged decline of the scorpion. At present, domestic oil and fat stocks are high and the market pressure is heavy. Without the support of the outer disk, the market may intensify the high level of shocks. It is advisable to use short-term participation or arbitrage between varieties.

V. Future market outlook and strategy recommendation

1, cockroaches: strong inside and weak weak beans and weak vegetables

The CBOT soybean market was mixed in October. The market expects that the supply and demand report for October will further increase the possibility of yield and production. Harvest pressure will be reflected. From a time perspective, the US Department of Agriculture reported that before October 12, the market may be weak, and harvesting lows may occur. With the digestibility of production, the late South American sowing weather and the export of US beans will support prices. For the domestic cockroach market, before the beginning of October, due to the long holiday and the 19th National Congress, some oil plants will be shut down, and soybean meal stocks will be reduced. Relatively speaking, since October is the weakest month for the consumption of rapeseed, the pattern of strong soybeans and weak vegetables will be highlighted. Relatively speaking, soybean meal is stronger than the vegetable meal, and the overall protein market is strong and weak; the soybean meal is strong and the vegetable is weak.

2, oil: stock pressure is greater than weak market, palm oil production rhythm changes are worthy of attention

Due to the frequent changes in the relevant policies of biodiesel in the United States, the market is also intensifying the divergence of future consumption expectations of US soybean oil. The Malaysian palm oil supply and demand report released in October became the key. If the Malaysian palm oil production dropped significantly in September, it means that the palm palm oil entered the production cycle ahead of schedule and the supply pressure was released. In contrast, domestic oil market inventory pressure remains evident in October, soy oil stocks may fall, but palm oil and rapeseed oil may increase. However, due to the steady domestic demand for oil in October. The oil and fat market destocking process is slow. Relatively speaking, due to the upside down of palm oil, there is still a gap in supply. Once the purchase is insufficient in the later period, it will boost the oil market.

3, strategy recommendation

Unilateral strategy: As the State Reserve temporarily stopped shooting soybeans, the previous soybean transaction rate was high, indicating that the soybean market price is more recognized, and soybeans will show a strong operation. It is recommended that investors treat the apes market in a range operation and operate in the interval band. Mainly. Grease is running weakly, paying attention to changes in rhythm.

Arbitrage strategy: You can buy bean empty operation; palm oil is stronger than soybean oil, and it is stronger than the future. Soybean oil is the opposite; this can be considered to buy palm oil near the moon and the moon, soy oil to buy near the moon and the moon.

Option strategy: In the medium and long term, we can also consider the strategy of doing more volatility.

Future market concerns: South American planting schedule and weather, North American sales progress, domestic oil plant crushing rhythm, Malay palm oil production inventory.

Big futures

Sina statement: Sina's posting of this article for the purpose of transmitting more information does not mean agreeing with its views or confirming its description. Article content is for reference only and does not constitute investment advice. Investors operate on this basis at their own risk.Enter [Sina Finance and Economics Unit] Discussion

Kids Running Clothes,Sporty Functional Clothings,Waterproof Cycling Jacket,Functional Clothings

Yangzhou Youju E-commerce Co.,Ltd , https://www.xiangyugarments.com