![<?echo $_SERVER['SERVER_NAME'];?>](/template/twentyseventeen/skin/images/header.jpg)

Last week, global oilseed prices continued their recent decline, mainly due to the overall good weather conditions in the South American soybean producing areas, boosting production prospects, and the US dollar exchange rate was firm, weakening the competitiveness of US agricultural exports. However, US soybean demand is still strong, restricting the downside of soybean prices.

The focus of the oilseed market this week is the weather in South America. Last weekend, Argentina's dry soybean producing area ushered in much-needed rainfall, and more rains appeared later this week, greatly improving the dry conditions, helping farmers to speed up soybean planting, and also benefiting the initial growth of soybean crops. . So far, the 2016/17 Argentine soybean planting work has been completed 66%, and the unevenness is consistent. Some farmers in central and southern Buenos Aires had suspended planting due to dry weather before the weekend rains. Rainfall during the weekend is enough to prompt farmers in the provinces of Buenos Aires and La Pampa to resume planting.

In Brazil, the weather situation in the soybean producing areas is generally good, so recently analysts have raised the Brazilian soybean production forecast data. Safrase Mercado raised its 2016/17 Brazilian soybean production forecast to 106.1 million tons, up from the previous forecast of 103.5 million tons. AgRural raised its soybean production forecast to 101.8 million tons, up from the previous forecast of 100.4 million tons. According to Safras, as of December 16, 2016, Brazil's 2016/17 soybean planting work has been completed 97.7%, up from 95.5% in the same period of last year, and basically not equal to the average annual growth rate of 97.5%. Mato Grosso, the number one soybean producing area, is still raining, which is conducive to the growth of soybean crops. At present, local soybean crops have begun to grow pods. Future concerns may be concentrated on excessive rainfall. It has been raining for five consecutive days in central Mato Grosso, and the rainfall in the past three months has exceeded normal levels. In the first half of December, rainfall in some areas was 7 to 8 inches, or even more. If this situation continues into January, it may cause problems in the early stages of soybean harvesting. At the end of December, the state of Mato Grosso will begin harvesting early sowing soybeans.

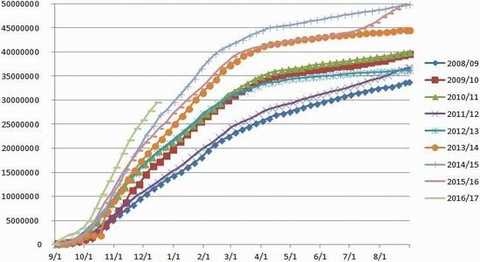

US soybean export demand, according to the weekly export sales report released by the US Department of Agriculture, as of the week of December 13, the US soybean export sales volume was 1.8 million tons, 10% lower than last week, but The four-week average is 9% higher. The data exceeded analysts' forecasts of 1.1 to 1.4 million tons. So far this year, the total US soybean export sales have reached 46.91 million tons, an increase of 26.8% over the same period of the previous year.

According to news from the official director, London's Sucden Financial Co. said that demand for soybeans is strong and may continue to support soybean prices in 2017. The US Department of Agriculture expects China's soybean consumption to reach a record 100.8 million tons this year. The company believes that strong demand prospects may cause soybean prices to stabilize at $10 per bushel in the short term and may rise further. However, once the South American soybean harvesting work is fully expanded, the price of beans may fall back to 9.50 US dollars per bushel. In addition, analysts are generally optimistic about the prospects for US soybean planting next spring, which may also put downward pressure on soybean prices.

The first part of the market review

Figure 1CBOT soybean main

Figure 2 Bean A1705

Figure 3 Cardamom M1705

Figure 4 dish 粕 RM705

The second part is the analysis of the fundamentals of mites

1. Weekly export sales report (WeeklyExportSales)

The USDA export sales report shows that as of December 15th, US soybean export sales were 1.8 million tons, 10% lower than last week, but 9% higher than the four-week average. The data exceeded analysts' forecasts of 1.1 to 1.4 million tons. So far this year, the total US soybean export sales have reached 46.91 million tons, an increase of 26.8% over the same period of the previous year.

Figure 5 US soybean export sales progress (unit: tons)

Source: USDA, Cinda Futures R&D Center

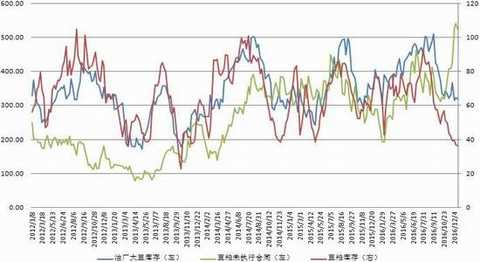

2. CFTC commodity fund positions

According to the report of the US Commodity Futures Trading Commission (CFTC), as of December 20, the total holdings of commodity funds in CBOT soybean futures were 716,574 contracts, an increase of -26,072 contracts from December 13. Among them, the fund's long position was 224,360 lots, an increase of -16,222 lots; the fund's short position was 87,786 lots, an increase of -802 lots; the net long position was 136,574 lots, an increase of -15,420 lots.

Table 1 CFTC soybean total positions change (unit: hand)

Figure 6 CFTC soybean total position and fund net position (unit: hand)

Source: CFTC, Wenhua Finance, Cinda Futures R&D Center

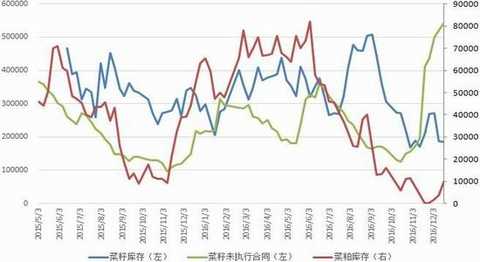

3, oil plant inventory and operating rate

In the 51st week of 2016 (ending December 18th), the inventory of soybeans in the oilfields of major coastal areas decreased slightly. The total stock of soybeans in Zhoukoukou was 3,195,100 tons, down 27,000 tons from last week, a decrease of 0.84. %, down 8.88% from the same period last year. In late December, the speed of soybean arrival will accelerate, but the rate of oil planting has also remained at a high level. It is expected that soybean stocks will not change much in the coming weeks. The rate of depreciation in oil plants dropped slightly, and the speed of picking up goods was faster, which caused the stock of soybean meal in the week to continue to decline slightly. This week, the turnover of soybean meal was less than that of last week, and the amount of unexecuted contracted soybean meal decreased. As of December 18, the total inventory of soybean meal in oilfields in major coastal areas was 363,500 tons, a decrease of 0.75 million tons from the previous week, a decrease of 2.02%, which was 42.55% lower than the same period of last year. When Zhou Douyu did not execute the contract of 5,217,500 tons, a decrease of 203,600 tons from last week, a decrease of 3.75%, an increase of 87.92% compared with the same period of last year, due to the hot sales of this year's basis. Next week, the oil planting rate will remain at a high level, while the terminal stocking speed will slow down. It is expected that the decline in soybean meal stocks will slow down, and there may be a slight rebound. However, the overall price will be at a low level and the supply of soybean meal will be tight. Mitigation will take a while.

Figure 7: Soybean stocks, soybean meal stocks and soybean meal unexecuted contracts in oil plants in coastal areas (unit: 10,000 tons)

Source: Tianxia Granary, Cinda Futures R&D Center

The stocks of rapeseed in the Guangdong-Guangdong and Fodi regions were 186,000 tons, an increase of -0.2 million tons from the previous week, an increase of -1.06%; the stock of oilseed meal in the oil plant was 10,000 tons, an increase of 16,200 tons from the previous week, an increase of 163.16%; The contract was 543,500 tons, an increase of 23,500 tons from last week, an increase of 4.52%. The total amount of rapeseed crushed was 75,700 tons, an increase of 20,000 tons from the previous week, an increase of 20.90%. The rate of rapeseed crushing was 15.77% this week, among which the domestic rapeseed oil plant had a drop rate of 0.4% this week. The factory has a probability of 26.70%. Some oil plants will have downtime plans next week, and the crushing volume will drop to about 70,000 tons.

Figure 8 Number of stocks and unexecuted contracts of Liangguang and Fujian Oil Plants (unit: ton)

Source: Tianxia Granary, Cinda Futures Research Center

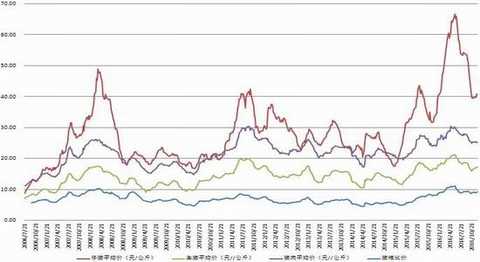

4, pig breeding

The pig price was adjusted in a narrow range this week. At the beginning of the week, the price of pigs rose and fell, but as the boost effect was lost after the winter solstice, the slaughter volume declined and the pig price showed a downward trend again. However, the current market for pigs in Beibei has not yet started, and the demand for bacon production in some areas of Nanxun has declined. The market output of the market has increased since the winter solstice, and the willingness of the slaughter enterprises to increase prices has increased. However, the supply fundamentals are tightening, and the weather is affected by the weather. In some areas, the production and transportation of pigs are blocked. However, when New Year’s Day is approaching, the market demand for fresh food is increasing, and the price of slaughtering enterprises is not increasing. .

The price of live pigs was 16.96 yuan / kg, up -0.1% from the previous month and up 4.04% year-on-year. At the end of the winter solstice stocking, the purchase of pigs from slaughtering enterprises decreased, and the price of pigs was stable.

The piglet price was 43.54 yuan / kg, up -1.2% from the previous month and up 27.4% year-on-year. The breeding market has slowly recovered, the number of piglets has increased, and the price of piglets has continued to decline.

The price of pork market fell to 27.48 yuan / kg, up -0.2% from the previous month and up 5.9% year-on-year. After the winter solstice, the demand for pork has weakened, the purchases of slaughter companies have decreased, and the price of meat has been adjusted slightly.

The price of pig food rose to 9.5:1, up 3.1% from the previous month and up 15.4% year-on-year.

Figure 9 Average price of piglets, pigs and pork in 22 provinces and cities in China

Source: China Animal Husbandry Information Network, Cinda Futures R&D Center

Cinda Futures Xing Cheng

Sina statement: Sina's posting of this article for the purpose of transmitting more information does not mean agreeing with its views or confirming its description. Article content is for reference only and does not constitute investment advice. Investors operate on this basis at their own risk.

Rectangle Cushion,Sofa Pillow Covers,Green Cushion Covers,Waterproof Cushion Covers

Nantong NATASHA Textiles Co.,Ltd. , https://www.ntnatashatextile.com